In the world of finance, your credit score is like your financial resume, showcasing your ability to manage debt and repay loans. A good credit score not only opens the door to better loan rates but also reflects your financial responsibility and trustworthiness. If you’re looking to improve your credit score and secure better loan rates, look no further. This article will provide you with practical tips and strategies to boost your credit score and set yourself up for financial success. Let’s dive in and unlock the secrets to improving your credit score!

Understanding the Factors Affecting Your Credit Score

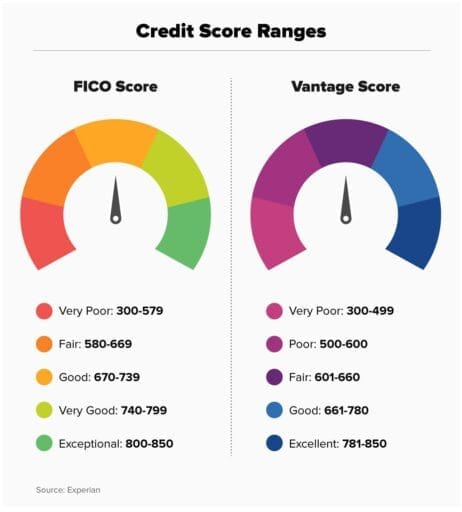

Having a good credit score is essential for obtaining favorable loan rates. Several factors influence your credit score, and understanding them can help you improve it. One key factor is payment history. Late payments or missed payments can negatively impact your score. Make sure to pay your bills on time to maintain a good credit history.

Another factor affecting your credit score is credit utilization. This refers to the amount of credit you’re using compared to your total available credit. Aim to keep your credit utilization below 30% to demonstrate responsible credit management. Additionally, the length of your credit history, types of credit accounts, and new credit applications also play a role in determining your credit score. By being mindful of these factors and making proactive changes, you can work towards improving your credit score and securing better loan rates in the future.

Effective Strategies for Building Credit History

Building a solid credit history is essential for securing favorable loan rates and financial opportunities. To improve your credit score, consider implementing the following effective strategies:

- Pay Your Bills on Time: Timely payments are crucial for demonstrating responsible financial behavior to creditors.

- Keep Your Credit Utilization Low: Aim to use only a small portion of your available credit to show restraint and financial discipline.

- Diversify Your Credit Mix: Having a mix of credit accounts, such as credit cards and loans, can showcase your ability to manage different types of debt.

| Strategy | Impact |

|---|---|

| Pay Bills on Time | Positive Payment History |

| Keep Credit Utilization Low | Improves Credit Score |

| Diversify Credit Mix | Enhances Credit Profile |

By incorporating these strategies into your financial routine, you can gradually build a strong credit history and increase your credit score. This, in turn, will open doors to better loan rates, improved financial products, and overall financial security for your future.

Smart Tips for Maintaining a Good Credit Score

Improving your credit score is essential if you want to secure better loan rates. One smart tip is to make sure you pay your bills on time every month. Late payments can significantly impact your credit score, so setting up automatic payments or reminders can help you stay on track. Additionally, keeping your credit card balances low and avoiding maxing them out can also boost your credit score.

Another tip for maintaining a good credit score is to regularly check your credit report for errors. Mistakes on your report can drag down your score, so it’s important to review it at least once a year. In addition, diversifying the types of credit you have, such as a mix of credit cards and loans, can demonstrate to lenders that you are a responsible borrower. By following these smart tips, you can improve your credit score and increase your chances of qualifying for better loan rates in the future.

Utilizing Credit Score Improvement Tools and Resources

One way to improve your credit score and secure better loan rates is by utilizing various credit score improvement tools and resources available to you. These tools can help you better understand your credit history, identify areas for improvement, and take actionable steps towards boosting your score.

Some helpful tools and resources to consider include:

- Credit monitoring services: Stay informed about changes to your credit report and receive alerts for potential fraudulent activity.

- Debt management tools: Create a plan to pay down debt and improve your credit utilization ratio.

- Budgeting apps: Track your spending habits and identify areas where you can save money to put towards paying off debt.

Future Outlook

In conclusion, taking steps to improve your credit score can open up a world of opportunities when it comes to loan rates and financial stability. By following the tips outlined in this article and staying committed to managing your credit wisely, you can set yourself up for success in the long run. Remember, your credit score is a reflection of your financial responsibility, so make sure to always be mindful of your spending habits and prioritize making timely payments. With a little effort and patience, you can achieve the credit score you desire and enjoy the benefits of better loan rates in the future. Good luck on your journey to financial well-being!